Growth

Zero Tax on ₹17 Lakh Rental Income? Here’s How It Works

Written by

Shivanshi Dheer

Read Time

6 min read

Posted on

April 29, 2026

Overview

Overview

Zero Tax on ₹17 Lakh Rental Income? Here’s How It Works

A Bengaluru CA’s LinkedIn post went viral for revealing a perfectly legal combination of Section 24(a) and Section 87A that can wipe out your entire rental tax bill to zero tax – no receipts required.

“The tax code isn’t broken. Most people just don’t read it carefully enough.”

That’s what Bengaluru-based Chartered Accountant Kanan Bahl wrote on LinkedIn – and it set off a firestorm of comments, shares, and disbelief. The claim: a landlord earning ₹17 lakh a year in rent can owe exactly ₹0 in income tax. Legally. Without juggling investments or submitting a single repair bill.

Is it a loophole? A privilege of the rich? Or just a tax code that most people never bother to understand? Let’s break it down – every step, every number, every condition.

Step 1 · The Foundation

Rental Income Is Taxed Differently

When you earn a salary, it’s taxed as “Income from Salaries.” When you rent out a property, the Income Tax Act places it under a separate bucket: “Income from House Property.” This distinction matters enormously, because this head comes with its own set of deductions that don’t exist anywhere else in the tax code.

The most powerful of these is Section 24(a) – a flat 30% standard deduction on your Net Annual Value (NAV). You don’t need to prove anything. No bills for painting the flat, no plumber’s receipts, no maintenance logs. The government simply assumes that 30% of your rental income goes toward property upkeep and gives it to you automatically.

💡Why does this deduction exist?

Because rental properties genuinely incur costs – repairs, maintenance, property taxes, wear and tear. Rather than making every landlord document each expense, the law grants a blanket 30% deduction. Simple, clean, and universally available to all property owners.

Step 2 · The Calculation

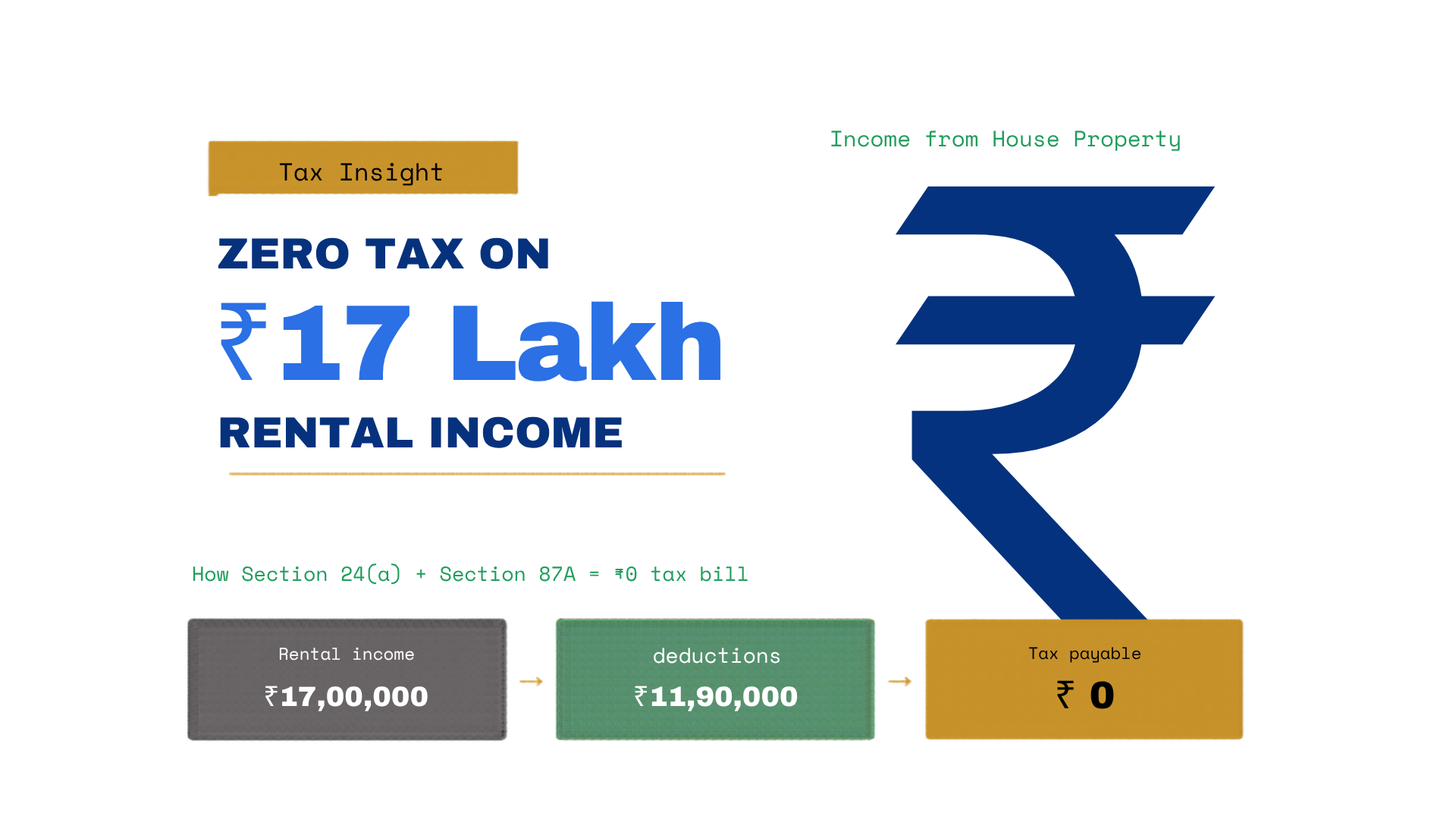

How ₹17 Lakh Becomes ₹11.9 Lakh and Then Zero Tax?

Let’s see the complete tax working – FY 2025-26

Gross Annual Rental Income = ₹17,00,000

Less: Municipal Taxes Paid = ₹0

Net Annual Value (NAV) = ₹17,00,000

Section 24(a) Standard Deduction (Flat 30% – No Bills Needed)= – ₹5,10,000

Taxable Income from House Property = ₹11,90,000

Income Tax on ₹11.9 Lakh (New Regime Slabs) ≈ ₹59,000

Section 87A Rebate Taxable income ≤ ₹12 Lakh = – ₹59,000

Net Tax Payable = ₹ 0

The magic is in the sequencing. After Section 24(a) trims ₹17 lakh down to ₹11.9 lakh, the new tax regime slabs produce a tax liability of roughly ₹59,000. Then Budget 2025-26’s enhanced Section 87A rebate steps in – it fully cancels out any tax liability up to ₹60,000 for taxpayers with income below ₹12 lakh. The numbers land almost perfectly.

Step 3 · The Fine Print

Three Conditions That Must All Be True

This is where many people get tripped up. The zero-tax outcome is real, but it doesn’t apply universally. Three specific conditions must be satisfied simultaneously:

- Rental Is Your Primary Income

This works when rental income is your dominant or sole income source. If you also draw a salary or earn significant business income, that gets added to the total – and the combined figure may push you well past ₹12 lakh, killing the 87A rebate eligibility entirely. - You Opt for the New Tax Regime

The enhanced 87A rebate (up to ₹60,000) is exclusive to the new regime in FY 2025-26. The old regime only offers a ₹12,500 rebate on income up to ₹5 lakh – nowhere near enough to cancel out the tax here. You must explicitly choose the new regime while filing your ITR. - Income Classification Is Correct

The rent must genuinely qualify as “Income from House Property.” If the tax department reclassifies it as business income – which can happen when renting is your primary commercial activity – different rules apply, and Section 24(a)’s flat 30% deduction is off the table.

Which Tax Regime is best for you?

Old vs. New: Which Works Better for Landlords?

This is a scenario where the new regime clearly wins for the specific ₹17 lakh rental income profile. Here’s a side-by-side view:

| Factor | New Regime |

|---|---|

| Section 24(a) 30% deduction available? | ✓ Yes — Still available for let-out property |

| Section 87A rebate limit | ₹60,000 (income up to ₹12 lakh) |

| Home loan interest deduction (let-out) | ✗ Not available |

| 80C / 80D deductions | ✗ Not available |

| Net tax on ₹17L rental (no other income) | ₹0 |

| Best suited for | Pure rental income with no major deductions to claim |

If you have a large home loan on your let-out property, or significant 80C investments, revisit the old regime calculation with a CA. The new regime’s zero-tax outcome only makes sense when you don’t have large deductions being left on the table.

Common Mistakes That Can Stop You From Paying Zero Tax

Forgetting other income sources. Interest on savings accounts, fixed deposits, dividends – all of these get added to your total income. If your FD interest alone is ₹80,000, your taxable income crosses ₹12 lakh, and the Section 87A rebate vanishes. Check your Form 26AS carefully before assuming zero liability.

Assuming it works for special-rate income. The Section 87A rebate does not apply to income taxed at special rates – such as short-term or long-term capital gains. Rental income taxed under house property is regular income and qualifies, but mixing it with capital gains can complicate matters.

Not filing your ITR. The rebate doesn’t apply automatically by magic. You must file your Income Tax Return, select the new regime, and accurately report your rental income and deductions. The benefit is claimed through the ITR filing process.

Documentation is the one condition fully in your control. RentOk generates rent receipts, tracks payment history, and keeps your records organised – exactly what your CA will ask for at filing time

The 87A marginal relief note ⚠️ : If your taxable income is, say, ₹12.05 lakh – just above the threshold – you don’t suddenly owe full tax. A marginal relief provision ensures that the extra tax you pay does not exceed the extra income above ₹12 lakh. So a small overshoot isn’t catastrophic, but the full zero-tax outcome only works cleanly at ₹11.9 lakh and below.

What is the Bigger Picture here?

This Isn’t a Loophole. It’s the Design.

When the Bengaluru CA’s LinkedIn post went viral, many reactions swung between two extremes: “this is unfair” and “this is incredible.” But neither quite captures what’s actually happening here.

Section 24(a)’s flat 30% deduction has existed for decades. It was always there to simplify compliance for landlords who would otherwise need to track every maintenance expense. Section 87A’s enhanced rebate was explicitly designed by Budget 2025-26 to make the new tax regime more attractive and to provide meaningful relief to middle-income taxpayers.

As Kanan Bahl put it in her post: “The tax code isn’t broken. Most people just don’t read it carefully enough“.

The zero-tax outcome at ₹17 lakh isn’t a design flaw – it’s a design feature that works when the law’s intent aligns with your income profile. The CA didn’t discover a workaround; she read the statute carefully enough to see how its parts fit together.

Disclaimer: This article is written for informational and educational purposes only, based on publicly available tax provisions for FY 2025–26. Individual tax situations vary significantly based on total income, income sources, applicable deductions, and residential status. The zero-tax outcome described here applies under specific conditions and may not apply to your personal circumstances.

Always consult a qualified Chartered Accountant or tax advisor before making decisions based on this information.

RentOk also offers CA and Accounting services. Just let us know, and we’ll take care of the rest.

About the Author

Shivanshi Dheer

Shivanshi Dheer sharing actionable strategies and information on PG/hostel management to help simplify renting and scale with RentOk.